.png)

In Dallas-Fort Worth, creative capital structures are only as strong as the leases supporting them. Seller financing, private lending, and bespoke capital stacks work on paper, but they perform in practice only when the underlying leases function as reliable credit assets rather than moving targets.

Higher base rates and tighter bank credit have pushed DFW sponsors deeper into seller financing, private lenders, and custom capital stacks, particularly across small-to-mid cap industrial, retail, and office assets. In a market that added roughly 100 residents per day and crossed 8 million people by 2024, transaction velocity in neighborhood retail, flex industrial, and small office trades has accelerated. Buyers who can close quickly with flexible capital have a structural advantage.

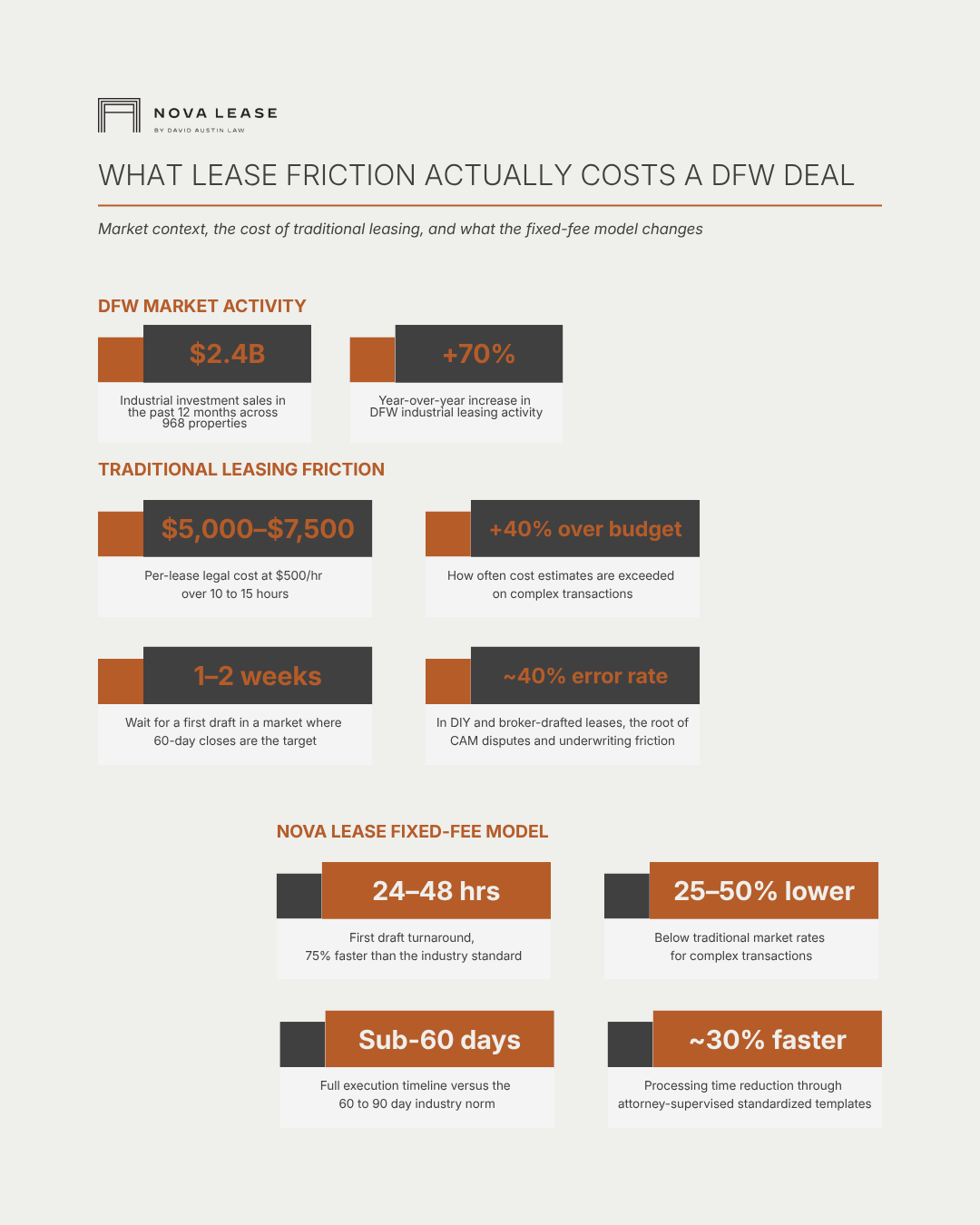

Industrial illustrates the dynamic clearly. Over the past 12 months, DFW industrial investment sales totaled approximately $2.4 billion across 968 properties at an average 6.4% cap rate, with leasing activity up more than 70% year-over-year. That volume of smaller transactions is precisely where seller-financed notes and private lenders fill the gap, but only when cash flows and legal structures are transparent enough to support fast, confident underwriting.

In most of these transactions, the real risk isn't the capital stack. It's the leases.

Walk into a typical small commercial acquisition in DFW and the same pattern appears: broker-drafted forms with incomplete CAM definitions, conflicting escalation formulas across documents from multiple firms, and multiple "final" versions with no clear indication which one controls. Diligence extends. Counsel costs inflate. When a handful of tenants drive the entire income profile, as is common in strip retail or shallow-bay industrial, an $8,000 CAM dispute can represent nearly 3% of NOI. That's a material hit for both sponsor and seller-lender.

For seller financing and private lending, that ambiguity carries a concrete price. A seller carrying a note or a private fund providing senior debt must underwrite rent roll quality, enforcement rights, and expense recoveries. When leases are inconsistent, the response is predictable: spreads widen, LTV drops, or the lender exits. The economics that made seller financing attractive on paper get eroded by legal uncertainty long before funding.

Creative capital structures amplify the cost of delay in ways conventional financing does not. A sponsor closing a seller-financed DFW industrial asset in 60 days has fundamentally different risk tolerance for legal drift than a core fund with a 120-day window and cheap balance sheet capital. Traditional Dallas leasing counsel typically charges around $500 per hour, with 10 to 15 hours per lease. That translates to $5,000 to $7,500 per negotiation and frequently runs 40% over initial estimates in complex situations.

That unpredictability falls hardest on seller-financed and privately funded deals because the legal budget comes directly out of the sponsor's spread or the seller's proceeds, not an institution's overhead line. Every week of delay also shifts negotiating leverage toward tenants and raises the probability that a key occupant re-trades or walks.

Nova Lease addresses a specific, high-impact segment of the risk stack: it standardizes leases and removes volatility from the legal execution process.

Attorney-supervised templates built around current market terms create consistency in NNN definitions, expense caps, options, and co-tenancy provisions across an entire portfolio. That standardization reduces processing time by roughly 30% and cuts error rates that can approach 40% in DIY or broker-drafted leases, which is precisely where disputes originate and underwriting friction compounds.

On cost, flat-fee pricing runs typically 25 to 50% below traditional market rates for complex transactions. Organizations using the model report 40 to 60% overall savings on lease-related legal spend. Because those fees are fixed and tied to defined scopes rather than measured in six-minute billing increments, they function as a budgetable line item. Sponsors who know their lease expirations and projected activity can forecast their annual leasing cost with real precision.

Speed is the other variable. First drafts are delivered within 24 to 48 hours rather than the industry norm of one to two weeks, a roughly 75% reduction in drafting time that enables sub-60-day execution in markets where traditional approaches routinely consume 60 to 90 days. For seller-financed and privately funded DFW transactions, that compression shrinks the window in which tenants can change their minds, lenders can shift terms, or market conditions can move against the capital stack.

The market data makes the stakes concrete. DFW office vacancy sits around 25.1% overall, but Class A properties absorbed roughly 1.5 million square feet in Q1 2025 even as Class B space continued to lose demand. Rents for top-tier product hit record highs near the upper $30s per square foot, growing 2.8 to 9.2% year-over-year. In that bifurcated environment, landlords who execute leases faster and cleaner in strong buildings command better financing terms, whether from banks, private lenders, or sellers carrying notes.

Industrial reinforces the same point. With 7.7 million square feet of quarterly net absorption and $2.4 billion in annual sales volume at an average 6.4% cap rate, DFW's logistics market is deep but increasingly selective about operator quality. Sellers willing to carry paper and private funds writing loans in this segment care about the reliability of lease income. Standardized, attorney-supervised documents and predictable legal costs help sponsors justify tighter spreads and higher proceeds in competitive situations.

The through-line across both asset classes is the same: execution infrastructure is what separates sponsors who win deals from those who lose them at the finish line.

For institutional managers running DFW strategies that rely on seller financing or private credit, the operational takeaway is direct.

Nova Lease's fixed-fee leasing doesn't reprice the note, but it stabilizes the legal inputs that feed into every underwriting decision. Cycle time becomes a known quantity. Per-lease legal spend becomes a known quantity. Lease-level surprises become materially less likely. That stability lets both sponsors and lenders concentrate on underwriting actual credit and market risk, rather than holding reserves for documentation inconsistencies and process unpredictability.

That's the real value proposition: not cheaper legal work, but a leasing process that behaves like infrastructure rather than a variable. In a DFW market where capital is competing hard across industrial, retail, and office assets, the sponsors who close consistently aren't always the ones with the lowest cost of capital. They're the ones who've eliminated the friction that kills deals quietly, in due diligence, in negotiations, and in the final sprint to funding.