.png)

A Dallas office landlord signs a modified gross lease in 2019 at $32 per square foot. The pro forma models fine. Then insurance premiums jump 43% following Winter Storm Uri, property taxes surge as corporate relocations drive Uptown valuations higher, and utilities climb. Nobody carved out insurance or taxes when the deal was drafted. By year three, that landlord is absorbing hundreds of thousands in unrecoverable OpEx annually, money that was in the model and isn't in the bank.

That scenario is playing out across DFW right now, not because landlords made poor leasing decisions, but because the cost environment has shifted materially since 2019 and the lease structures haven't kept up. The question isn't whether NNN is better than gross. It's whether your current lease structure was designed for the cost environment you're actually operating in.

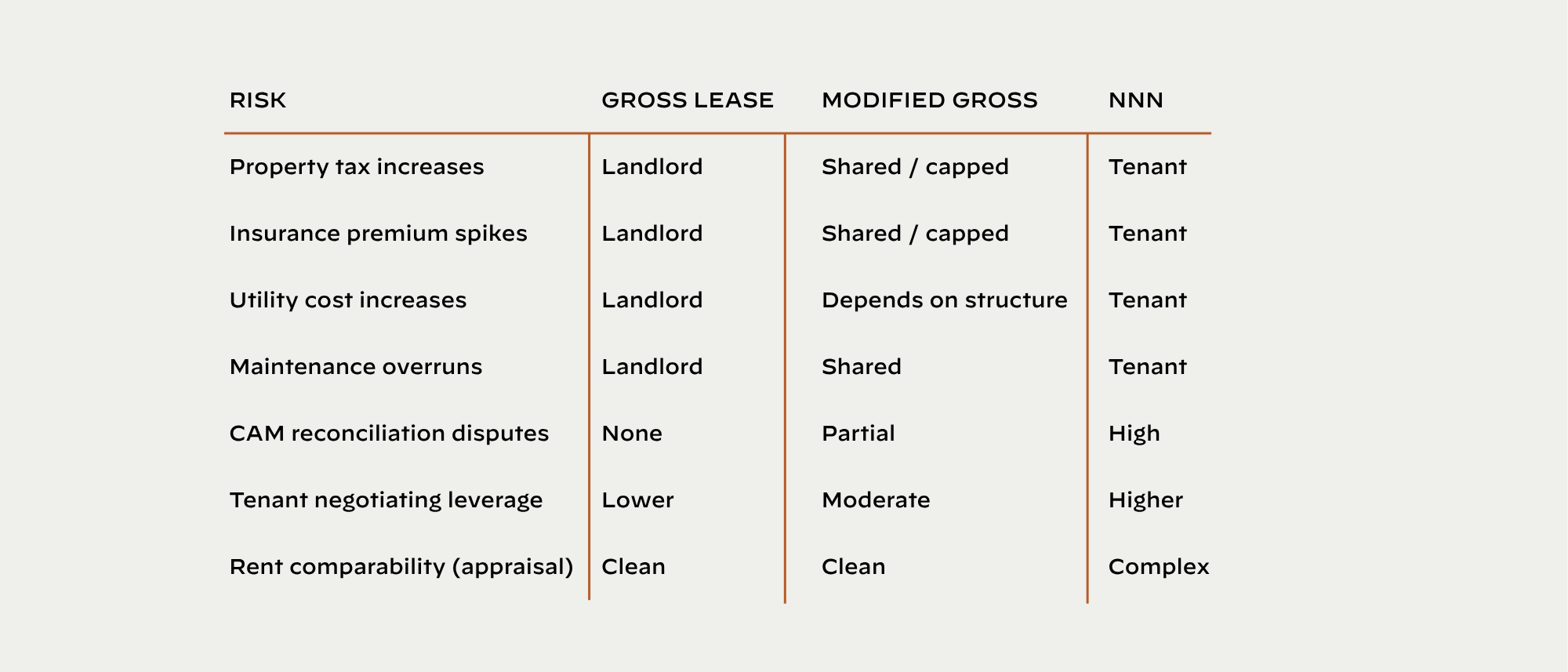

Most landlords know the definitions. The risk allocation those definitions produce, and how it performs when costs move, gets less attention.

Commercial property insurance premiums have increased an average of 7 to 11% annually since 2017, with spikes of 30 to 150% on specific DFW assets following weather-related losses. Insurers have repriced Texas wind, hail, and freeze risk permanently. For a landlord holding a gross lease on a 100,000 square foot building with a $400,000 annual insurance bill, a 40% increase represents $160,000 absorbed directly from NOI with no pass-through mechanism. A NNN landlord passes that entirely.

In Uptown, Las Colinas, and Frisco, appraisal increases of 15 to 30% in a single reappraisal cycle have not been unusual as corporate relocations drove valuations sharply higher. Landlords who locked in modified gross leases with tax expense caps between 2017 and 2019 are now absorbing the gap between their capped pass-through and actual tax liability, running $2 to $4 per square foot annually on assets where flat growth was assumed. On a 100,000 square foot building, that's $200,000 to $400,000 per year in unrecoverable cost.

Post-Uri grid reliability concerns are pushing landlords toward backup infrastructure investments, including generators, battery storage, and demand management systems, that create ongoing OpEx. Utility costs that were predictable line items in 2018 now carry real variance risk, and that variance doesn't disappear from the ledger; it just determines whose ledger it lands on. In gross leases, it sits entirely with the landlord. In NNN structures, it passes through, but only if the CAM accounting is clean and defensible enough to survive tenant audit, which is a drafting and operational discipline problem, not a structural one.

The gross lease that penciled in 2019 was underwritten against a cost environment that no longer exists.

Shifting to NNN solves the OpEx exposure problem but introduces its own operational risks that landlords need to price in honestly. CAM disputes are the most common: NNN leases shift costs to tenants only when the reconciliation process is clean and defensible, and tenants with sophisticated counsel will audit. Landlords with inconsistent expense allocations or vague CAM definitions face dispute risk that delays collections, strains tenant relationships, and in worst cases triggers termination claims. The answer is tight drafting and disciplined accounting, not avoidance of NNN structures, but the discipline is real.

Leasing velocity is the other variable. Credit tenants in Class A DFW office increasingly prefer modified gross structures because they want cost certainty for their own P&L forecasting. A landlord insisting on full NNN in a competitive market may lose deals to a competitor offering modified gross with well-defined pass-throughs. Structure is a leasing tool as much as a financial one.

Modified gross leases aren't the problem; poorly drafted ones are. A well-structured modified gross delivers most of NNN's OpEx protection without NNN's leasing friction. Four provisions determine whether the structure holds:

Insurance, property taxes, and utilities should pass through at 100%, uncapped. Capping them alongside janitorial and landscaping defeats the purpose entirely.

Not a favorable historical year, and not a partially occupied year that artificially deflates the baseline. Include reset language for major capital events or ownership transfers.

Occupancy-sensitive expenses should be grossed up to 95% occupancy for pass-through purposes, preventing tenants from benefiting from vacancy-driven cost deflation unrelated to property performance.

Annual reconciliation with a 90 to 120 day delivery requirement and a defined 90-day tenant audit window limits disputes and creates bilateral accountability.

The difference between a modified gross lease that leaks NOI and one that protects it is almost entirely in how "controllable expenses" was defined.

The landlord who defaults to gross because it's easier to lease, without modeling OpEx exposure across the full lease term, is making a financial decision without doing the financial analysis. In the current cost environment, that gap is measurable and it compounds.

Getting the structure right requires counsel who understands both sides of the ledger, meaning the legal mechanics and the asset management implications of every expense definition, cap, and carve-out in the document. In a DFW market where insurance, taxes, and utilities are all moving in one direction, the landlords who got this right before signing are outperforming the ones who are figuring it out now. Nova Lease was built to close that gap.